Extended Stay America Reports Filed Proxy Materials Related To Blackstone, Starwood Capital Deal

Author: Benzinga Newsdesk | April 26, 2021 08:10am

Sets June 8, 2021 as Special Meeting Date to Vote on the Transaction

Letter to Shareholders Highlights Immediate, Compelling and Certain Value of the Transaction that is Superior to Execution of Standalone Plan

Says Future Value Creation Beyond Transaction Price Would Require Flawless Execution and Significant Multiple Re-Rating

Underscores Transaction Price at 50%+ Premium to Pre-Pandemic Share Price Already Reflects Substantial Credit for Strategic Plan and Post-Pandemic Recovery

CHARLOTTE, N.C., April 26, 2021 (GLOBE NEWSWIRE) -- Extended Stay America, Inc. (“ESA”) and its paired-share REIT, ESH Hospitality, Inc. (“ESH” and, together with ESA, “Extended Stay” or the “Company”) (NASDAQ:STAY) today announced that it has filed a definitive joint proxy statement in connection with the Company’s previously announced definitive agreement to be acquired by a 50/50 joint venture between funds managed by Blackstone Real Estate Partners (“Blackstone”) and Starwood Capital Group (“Starwood Capital”) for $19.50 per paired share in an all-cash transaction valued at approximately $6 billion.

Extended Stay’s Special Meetings of Shareholders are scheduled to take place on June 8, 2021 at 8:30 A.M. Eastern Time for ESA and at 9:30 A.M Eastern Time for ESH. All shareholders of record of Extended Stay paired shares as of the close of business on April 19, 2021 will be entitled to vote their shares either in person or by proxy at the shareholder meetings.

The Company will commence mailing the joint proxy statement to its shareholders on or about April 26, 2021 and urges them to vote the WHITE card “FOR” the transaction.

The Company also sent the following letter to shareholders.

Dear Valued Shareholder,

The Special Meetings of Shareholders to vote on the proposed sale of Extended Stay America, Inc. (“ESA”) and its paired-share REIT, ESH Hospitality, Inc. (“ESH” and, together with ESA, “Extended Stay” or the “Company”) (NASDAQ:STAY) are scheduled for June 8, 2021, and your vote is extremely important no matter how many or how few shares you own.

We are writing to you as Board Chair and CEO to remind you that your vote “FOR” the transaction on the WHITE proxy card is critical to protecting your $19.50 per paired share in cash – an opportunity to realize immediate, certain and compelling value. The proxy statement included with this letter outlines the background of the transaction and the reasons the Boards of Directors of the Company strongly support the transaction, which include:

- Immediate, certain and compelling value to shareholders

- Superior value to the continued execution of Extended Stay’s strategic plan on a time and risk-adjusted basis

- Culmination of thorough actions to explore value-enhancing alternatives

The Blackstone / Starwood Capital transaction values our paired shares at more than a 50% premium to their pre-pandemic value and creates a compelling opportunity for shareholders to immediately realize the future benefits of our strategic initiatives.

We are incredibly proud of the Extended Stay team’s accomplishments over the past year, which have been recognized by the market and have contributed to our substantial outperformance during the pandemic. These accomplishments have positioned us to achieve this compelling valuation for our shareholders.

Our recommendation reflects careful consideration of all of the alternatives available to the Company to maximize shareholder value, including continuing to pursue our strategic plan and the Boards’ thorough efforts reviewing strategic alternatives over the years. Moreover, as our proxy statement more thoroughly describes, the Boards have extensively explored ways to enhance value for shareholders, both organically and inorganically, over our life as a public company.

As a result, our Boards have a well-informed and realistic assessment of a full range of value enhancing alternatives together with their potential benefits and risks, and determined that this transaction, with its significant premium over both our pre-pandemic and pre-announcement share price, to be in the best interests of all of our shareholders.

Immediate, certain and compelling value to shareholders

- The transaction provides a significant premium to shareholders

At $19.50 per share, the transaction delivers a meaningful premium to shareholders across multiple time horizons, including at the high end of precedent REIT transactions based on the trailing 30-trading day VWAP, 3-month VWAP and 52-week high prior to announcement.1

The $19.50 per share all cash price represents a:

- 51% premium to the company’s pre-pandemic share price2

- 15% premium to the $16.94 closing price the day prior to the announcement

- 23% premium to the 30-trading day volume weighted average price

- 28% premium to the 3-month volume weighted average price

- 44% premium to the 6-month volume weighted average price

- 76% premium to the 12-month volume weighted average price

- 15% premium to the 52-week high closing price

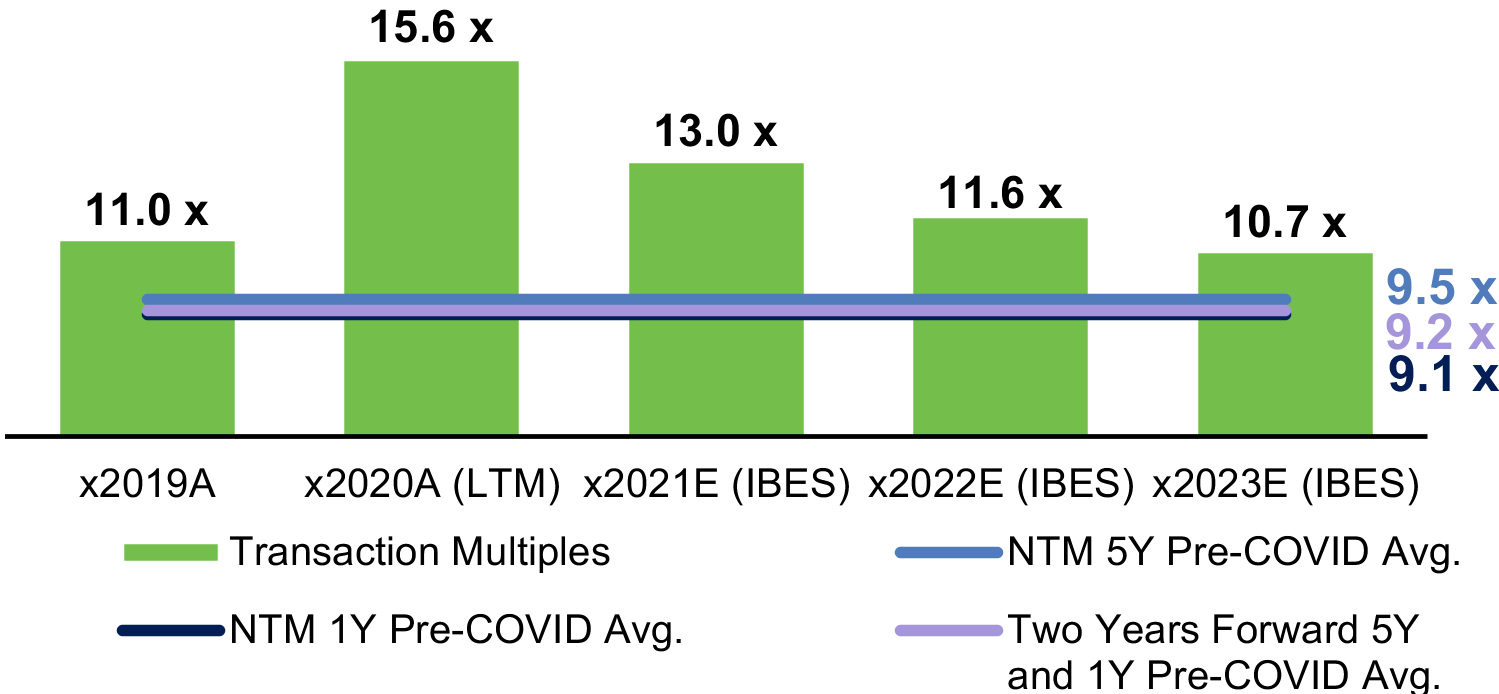

- The transaction represents a valuation well above Extended Stay’s historic EBITDA multiple

The transaction values the Company at 11.0x EBITDA for 20193, the most recently completed fiscal year prior to the pandemic, which reflects EBITDA that was 42% above that achieved in 2020, 19% above 2021 estimated consensus EBITDA and a level that is not expected to be achieved again until at least 2023, assuming successful implementation and execution of STAY’s strategic plan.

The transaction values the Company at 15.6x 2020 EBITDA, 13.0x 2021 estimated consensus EBITDA and 11.6x 2022 estimated consensus EBITDA. These represent significant premiums to where Extended Stay has consistently traded over its time as a public company, averaging a 9.5x NTM EBITDA multiple over the five years prior to the pandemic, and 9.1x NTM EBITDA for the year prior to the pandemic.4

Figure 1 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/5d8ae143-5a49-4d43-bda6-5e7601ddd177

The transaction provides superior value to the continued execution of Extended Stay’s strategic plan on a time and risk-adjusted basis

- The transaction provides certain value in place of execution risk

At the core of the Boards’ decision to endorse this transaction was an assessment of the risk-adjusted present value of the Company’s standalone business plan as the industry recovers from the pandemic, weighed against the certainty of $19.50 per share in cash today. The Boards believe this transaction delivers a meaningful premium to our shareholders as compared to our stand-alone plan on a risk adjusted basis.

The Boards, with the assistance of the management team and outside advisors, carefully evaluated the prospects of the Company’s standalone strategic plan and the execution risks inherent in multiple aspects of the plan. Specifically, the Boards considered the following factors based on management’s judgment, among other things:

- Significant Capital Needs: The magnitude of capital necessary to maintain and renovate the Company’s real estate assets and preserve the Company’s positioning as a mid-scale brand. The Company’s assets, which are on average more than 21 years old, have reached replacement age for many significant structural components requiring, in management’s view, a minimum investment of $750 million over the next three years, or approximately 50% of projected EBITDA over that same time period. This minimum investment represents an estimated amount necessary to achieve the revenue and EBITDA projections in the Company’s business plan and may not be sufficient in light of the size of prior renovation expenditures, the length of time since the last renovation program and the age of the properties. In particular, management’s plan calls for 2021-2022 capital expenditures of ~25% of revenue, which compares to ~17% historically (a ~40% increase on an average annual dollar basis). Approximately half of the 2021-2022 capital spend is associated with renovation projects, which drive EBITDA growth in management’s plan, but also comes with enhanced risk compared to maintenance capital;

- Expense Growth Pressures: Management’s outlook for property level performance, including both potential revenue gains and related cost considerations, with labor costs and certain other expenses facing above inflationary pressures. Notably, these expense pressures have weighed on the Company in the years prior to COVID with the Company’s EBITDA margins declining ~400 basis points from 2017 to 2019;

- Value Contribution from Asset Dispositions: A realistic assessment of the incremental value creation potential of the Company’s asset disposition program, which was informed by management’s extensive practical experience with the risks inherent in transactions that involve a conversion from a hotel to an alternative use. In addition, the Boards considered the uncertain multiple uplift from deployed sale proceeds as well as the substantial reduction in the Company’s revenue base, which would limit our ability to fully leverage our fixed cost structure; and

- Franchise Program Time Frame and Contribution: Expectations as to the size, EBITDA contribution, and significant length of time necessary to realize the financial impact from the Company’s franchise strategy.

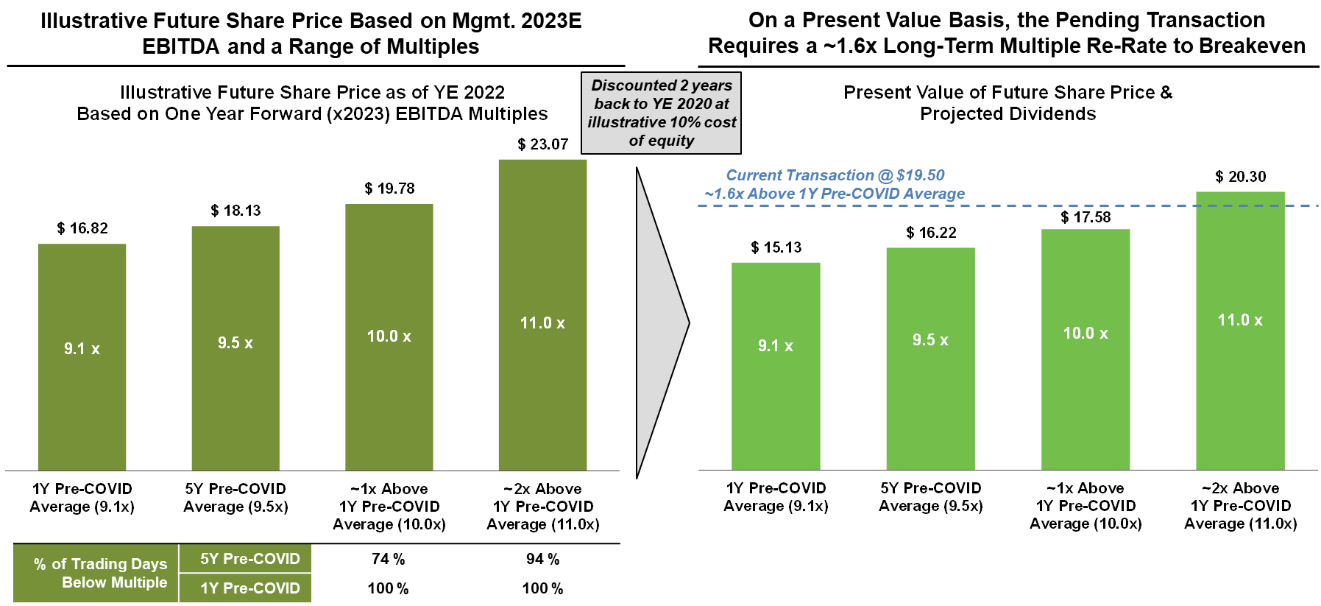

- Future value creation as an independent company would depend on the seamless execution of our strategic plan, coupled with achieving a significant multiple re-rating

The Boards’ analysis considered the present value of Extended Stay’s illustrative future share price, which is primarily a function of 1) projected EBITDA based on management’s plan, 2) future trading multiple (EV / EBITDA), 3) projected dividends and net debt and 4) discount rate.

The Boards’ analysis showed that in order to achieve a value per paired share in today’s dollars (i.e. present value) in excess of $19.50, STAY would need to achieve a full EBITDA recovery and realize significant revenue growth from commercial initiatives and capital investment, coupled with sustaining a trading multiple in the future in excess of 10.7x, representing a 1.6x increase to Extended Stay’s 1-year pre-COVID average EV / NTM EBITDA multiple of 9.1x.

Extended Stay has rarely traded at such a multiple in the past 5+ years and has never done so consistently. That is one reason why the Boards determined the certain $19.50 cash price from the Blackstone / Starwood Capital transaction represents a compelling opportunity for shareholders.

Figure 2 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/b60408ff-19cd-46e6-86d4-bdf7be068990

- STAY’s share price already reflects substantial post-pandemic uplift

Furthermore, while management and the Boards are gratified that shareholders and the market have recognized the value of the plan, it is the widely held consensus of the management team, Boards and their advisors that the market had already priced into the stock the achievement of the Company’s strategic plan to a substantial degree, despite the risks inherent in the recovery from a global pandemic or Company-specific execution risks.

The transaction marks the culmination of thorough actions to explore value-enhancing alternatives

- Prior strategic review processes yielded unattractive premia and limited buyer universe

Over the last four years the Company has conducted numerous private strategic review processes, none of which, in the Boards’ judgment, yielded compelling value alternatives for the Company's shareholders in comparison to the risk-adjusted value of management’s plan at the time. In each process where the Boards solicited and entertained offers for the whole Company, no credible bidders other than Blackstone and Starwood expressed an interest in acquiring the entire company.

No party has contacted the Company or its advisors to express any interest in exploring the possibility of a making a superior offer since the announcement of this transaction through the date of this letter. This is consistent with the Company’s experiences over the eight years the Company has been publicly traded.

- “OpCo/PropCo” transaction explored extensively, but determined to yield unattractive and uncertain risk-adjusted value creation vs. whole Company strategy

The Company’s Boards and management team have evaluated an OpCo/PropCo transaction extensively for several years, including the Boards’ comprehensive exploration in 2018-2019 of a transaction involving the sale of the OpCo and the REIT remaining as a standalone public company. At the conclusion of the process in May 2019, which resulted in only one credible proposal to acquire the OpCo, the Boards determined that a sale of the OpCo on the terms offered was not in the best interest of shareholders. The Boards determined that ceding control of the operations to a third party would create dis-synergies and introduce operational and financial risks, thus requiring meaningful PropCo multiple expansion in order to create sufficient value on a risk-adjusted basis. With the benefit of advice from its financial advisors, the Boards ultimately concluded that the likelihood of significant PropCo multiple expansion was highly uncertain, rendering the risk/return insufficient.

The Company has continued to periodically study the merits of an OpCo/PropCo transaction together with its advisors, including in connection with the contemplated transaction with Blackstone and Starwood Capital. Each time, including in recent months, the Boards concluded that pursuing such a transaction, in several alternative transaction structures, was not in the best interest of shareholders, particularly given the uncertainty associated with the potential trading value of a standalone REIT (90-95% of the company’s total enterprise value) and additional conflicts of interest that would be created, and especially in comparison to the 100% certainty of an all cash acquisition of the whole Company today.

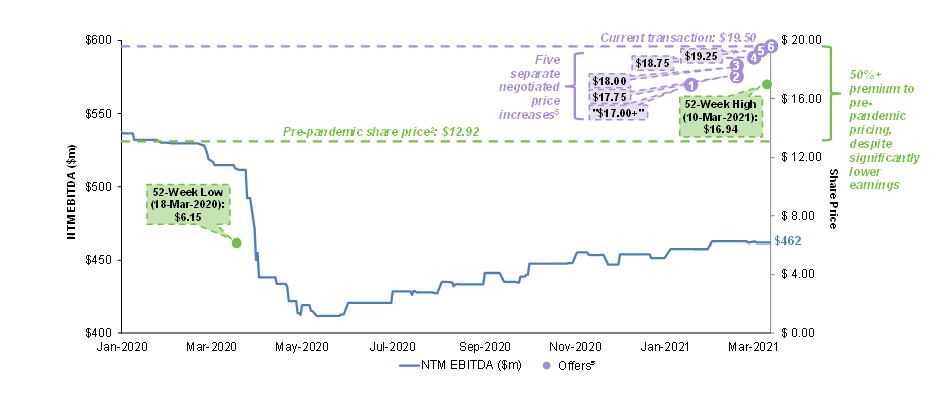

- Boards thoroughly negotiated with Blackstone and Starwood to reach this offer value

Blackstone increased the offer value on five separate occasions following the initial outreach at “$17.00+”, and the Boards only accepted the offer when they determined, in consultation with their advisors, that the offer was compelling, in the best interests of the shareholders and highly unlikely to be increased again (i.e. best and final).

The chart below illustrates that despite the decrease in STAY’s consensus NTM EBITDA projections to well below pre-pandemic levels, the Boards were able to achieve a price that was an approximately 50% premium to pre-pandemic levels through five rounds of price increases.5

Figure 3 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/bd01f3ed-350b-42da-be15-8593f6b50138

The Boards and management believe strongly that this is the right price, following the right process, at the right time, and thus is ultimately the right transaction to maximize value for all shareholders.

Your vote is extremely important, as a failure to vote will have the same effect as a vote against the transaction. No matter how many shares you own, we urge you to sign, date and return the enclosed WHITE proxy card and vote “FOR” the proposal to approve the transaction and secure your certain, immediate and compelling value of $19.50 per paired share in cash.

Please vote your WHITE proxy card today, either by Internet, telephone or mail. If you have any questions, or need assistance in voting your shares, please immediately contact Okapi Partners LLC, our proxy solicitor, at (877) 629-6357 (toll-free) or at info@okapipartners.com.

Sincerely,

Doug Geoga, Chairman of the Boards of the Company

Bruce Haase, President and Chief Executive Officer

Posted In: STAY