EverQuote Earnings Preview

Author: Benzinga Insights | October 31, 2025 02:01pm

EverQuote (NASDAQ:EVER) is gearing up to announce its quarterly earnings on Monday, 2025-11-03. Here's a quick overview of what investors should know before the release.

Analysts are estimating that EverQuote will report an earnings per share (EPS) of $0.48.

Investors in EverQuote are eagerly awaiting the company's announcement, hoping for news of surpassing estimates and positive guidance for the next quarter.

It's worth noting for new investors that stock prices can be heavily influenced by future projections rather than just past performance.

Overview of Past Earnings

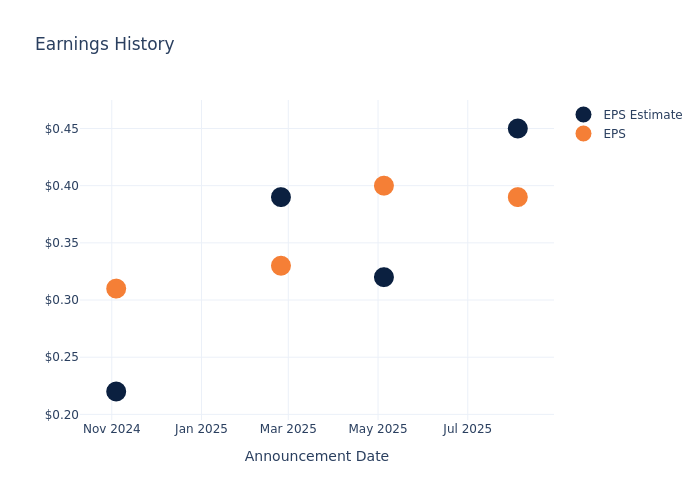

In the previous earnings release, the company missed EPS by $0.06, leading to a 7.76% drop in the share price the following trading session.

Here's a look at EverQuote's past performance and the resulting price change:

| Quarter |

Q2 2025 |

Q1 2025 |

Q4 2024 |

Q3 2024 |

| EPS Estimate |

0.45 |

0.32 |

0.39 |

0.22 |

| EPS Actual |

0.39 |

0.40 |

0.33 |

0.31 |

| Price Change % |

-8.00 |

-12.00 |

27.00 |

4.00 |

Tracking EverQuote's Stock Performance

Shares of EverQuote were trading at $20.65 as of October 30. Over the last 52-week period, shares are up 23.63%. Given that these returns are generally positive, long-term shareholders are likely bullish going into this earnings release.

Insights Shared by Analysts on EverQuote

For investors, grasping market sentiments and expectations in the industry is vital. This analysis explores the latest insights regarding EverQuote.

With 2 analyst ratings, EverQuote has a consensus rating of Buy. The average one-year price target is $34.0, indicating a potential 64.65% upside.

Peer Ratings Comparison

In this comparison, we explore the analyst ratings and average 1-year price targets of Getty Images Holdings, QuinStreet and Cars.com, three prominent industry players, offering insights into their relative performance expectations and market positioning.

- Analysts currently favor an Neutral trajectory for Getty Images Holdings, with an average 1-year price target of $4.12, suggesting a potential 80.05% downside.

- Analysts currently favor an Buy trajectory for QuinStreet, with an average 1-year price target of $24.0, suggesting a potential 16.22% upside.

- Analysts currently favor an Neutral trajectory for Cars.com, with an average 1-year price target of $17.2, suggesting a potential 16.71% downside.

Overview of Peer Analysis

The peer analysis summary outlines pivotal metrics for Getty Images Holdings, QuinStreet and Cars.com, demonstrating their respective standings within the industry and offering valuable insights into their market positions and comparative performance.

| Company |

Consensus |

Revenue Growth |

Gross Profit |

Return on Equity |

| EverQuote |

Buy |

33.71% |

$151.79M |

9.19% |

| Getty Images Holdings |

Neutral |

2.51% |

$169.25M |

-5.82% |

| QuinStreet |

Buy |

32.14% |

$27.85M |

1.34% |

| Cars.com |

Neutral |

-0.09% |

$148.19M |

1.44% |

Key Takeaway:

EverQuote ranks highest in Revenue Growth among its peers. It also leads in Gross Profit margin. However, it has a lower Return on Equity compared to some peers. Overall, EverQuote stands out for its strong revenue growth and gross profit performance within the group.

Delving into EverQuote's Background

EverQuote Inc is engaged in the business activity of offering an online marketplace for insurance shopping, connecting consumers with insurance provider customers, which includes both carriers and agents. The online marketplace offers consumers to find relevant insurance quotes based on car insurance, home insurance, and life insurance. The platform of the company is driven by data science. The firm's data and technology platform match and connects consumers seeking to purchase insurance with relevant options from its broad direct network of insurance providers. It derives a majority of revenue from Direct channels.

Unraveling the Financial Story of EverQuote

Market Capitalization Analysis: Falling below industry benchmarks, the company's market capitalization reflects a reduced size compared to peers. This positioning may be influenced by factors such as growth expectations or operational capacity.

Revenue Growth: EverQuote displayed positive results in 3 months. As of 30 June, 2025, the company achieved a solid revenue growth rate of approximately 33.71%. This indicates a notable increase in the company's top-line earnings. As compared to its peers, the company achieved a growth rate higher than the average among peers in Communication Services sector.

Net Margin: EverQuote's financial strength is reflected in its exceptional net margin, which exceeds industry averages. With a remarkable net margin of 9.39%, the company showcases strong profitability and effective cost management.

Return on Equity (ROE): EverQuote's ROE stands out, surpassing industry averages. With an impressive ROE of 9.19%, the company demonstrates effective use of equity capital and strong financial performance.

Return on Assets (ROA): EverQuote's ROA stands out, surpassing industry averages. With an impressive ROA of 6.21%, the company demonstrates effective utilization of assets and strong financial performance.

Debt Management: EverQuote's debt-to-equity ratio is below the industry average at 0.02, reflecting a lower dependency on debt financing and a more conservative financial approach.

To track all earnings releases for EverQuote visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.

Posted In: EVER